bank owned life insurance regulations

Financial institutions supervised by the Federal Reserve also engage in functionally regulated insurance. Banks are not permitted to hold life insurance in excess of their risk of loss or costs to be recovered.

:max_bytes(150000):strip_icc()/dotdash-insurance-companies-vs-banks-separate-and-not-equal-Final-9323c943f9974aad96b2c70d6e3aa577.jpg)

How Much BOLI Do Banks Own.

:max_bytes(150000):strip_icc()/P2-ThomasCatalano-d5607267f385443798ae950ece178afd.jpg)

. Bank Owned Life Insurance BOLI National banks may purchase and hold certain types of life insurance called bank-owned life insurance BOLI under 12 USC 24 Seventh. Act and Part 362 of the FDICs Regulations Attachments. A general rule of thumb for banks is to avoid holding BOLI in excess of 25 percent of its capital.

The federal banking agencies are providing guidance on the safe and sound banking practices they expect institutions to employ for the purchase and ongoing risk management of bank-owned life insurance. Banking organization insurance programs include the funding of employee benefits through purchases of corporate- or bank-owned life insurance and the transfer of insurable risks through coverages associated with risk management initiatives. The Office of the Comptroller of the Currency the Board of Governors of the Federal Reserve System the Federal Deposit Insurance Corporation and the Office of Thrift Supervision have issued the attached interagency statement on bank-owned life insurance BOLI to remind.

Related

Risk management processes for bank-owned life insurance BOLI are consistent with safe and sound banking practices. Some states also have specific laws in. The interagency statement also provides guidance for.

The bank is the owner of the policies pays all premiums typically a single lump-sum premium and is the beneficiary of the insurance proceeds. Written consent is obtained from all individuals to be insured. The general rule for bank-owned life insurance BOLI is that proceeds received by reason of death are tax free.

Individuals cannot purchase bank-owned life insurance for themselves. The interagency statement also provides guidance for. Bank Owned Life Insurance Rules and Regulations The Interagency Statement on the Purchase and Risk Management of Life Insurance OCC 2004-56 provides general guidance for banks and savings associations regarding supervisory expectations for the purchase and risk management for Bank Owned Life Insurance BOLI.

With the exception of term policies occasionally used to cover a borrower while a large debt remains outstanding bank-owned policies are usually permanent life insurance like whole or universal life. The federal banking agencies are issuing the attached Interagency. Risk management processes for bank-owned life insurance BOLI are consistent with safe and sound banking practices.

Bank-Owned Life InsuranceInteragency Statement on the Purchase and Risk Management of Life Insurance. The National Credit Union Administration NCUA allows for the purchase and holding to maturity of Credit Union Owned Life Insurance CUOLI products if it complies with 70119 of NCUAs rules regarding benefits for Federal Credit Union employees. BOLI is a life insurance policy purchased by a bank or bank holding company to insure the life of certain employees.

It should be noted that BOLIs current tax benefits have been unsuccessfully challenged over the years. Banks can purchase BOLI policies under 12 US. The bank is a direct creditor to the insurance company assets It is likely that the highest rated companies such as MassMutual Northwestern Mutual New York Life etc.

Code 24 Seventh. However if the BOLI policy is transferred for value ie the purchase of an existing policy rather than a newly issued policy the death benefit is no longer tax free unless an exception applies to the transfer. CUOLI may recover the cost of the employee benefit and the cost of the funding for that benefit.

Regulations restrict the insured to highly compensated employees typically directors and above or top 25 and the insured must provide consent. But if they are not grandfathered they may be surrendered for their cash surrender values. Some banks may choose to share a portion of these proceeds with plan participants.

As the name states COLI refers to life insurance that is purchased by a corporation for its own use. It is only for banks and corporations who purchase it for specific employees often executives. The permanent policies accrue cash value which earns tax.

Typically the insured employee is an officer or other highly compensated employee but a bank may purchase insurance for any employee. The guidance attached to this bulletin continues to apply to federal savings associations. Some state laws permit state-chartered banks to engage in activities including making investments that go beyond the authority of a national bank.

BOLI and other forms of life insurance investments provide tax-exempt income if the policy is held until the. How Bank-Owned Life Insurance Works. Hold BOLI assets according to the NFP-Michael White BOLI Holdings Report for Q3 2020.

Mirrors the insurance companies fixed income portfolio. Bank owned life insurance BOLI is life insurance purchased and owned by banks. Section 24 of the Federal.

3 Further guidance is found in section 101 j of the Internal Revenue Code and IRS Notice 2009-48. Interagency Statement on the Purchase and Risk Management of Life Insurance including Executive Summary. Two-thirds of banks in the US.

The bank purchases life insurance on a select group of management including officers or other key personnel. The cash surrender value of those policies totals 1822 billion. Bank Owned Life Insurance and Tax Reform.

Bank interest in bank-owned life insurance BOLI has been surging amid what some describe as a perfect storm of market conditions. If the tax treatment of Bank Owned Life Insurance BOLI changes existing plans may be grandfathered. Of the many tax law changes enacted as part of the Tax Cuts and Jobs Act of 2017 TCJA one provision is raising concern among banks involved in certain post-2017 acquisitions of target banks with ownership in bank-owned life insurance BOLI policies.

Would compare favorable to the best credits in the banks portfolio Misperception of the duration of BOLI. Since the bank owns the policy the bank receives the proceeds from the death benefit accrues revenue from investment. The corporation is either the total or partial beneficiary on the policy and an employee or.

The bank purchases life insurance on the lives of a group of employees such as executives and officers that participate in the banks benefit plans. The bank pays the premium owns the cash value of the policies and is the beneficiary of the insurance. Current regulations allow banks to take out life insurance on individuals they have an insurable interest in.

Banks can purchase BOLI policies in connection with employee compensation and benefit plans key person insurance insurance to recover the cost of providing pre- and postretirement employee. Risk of loss can be eliminated if a key employee no longer qualifies due to retirement resignation or a change of duties.

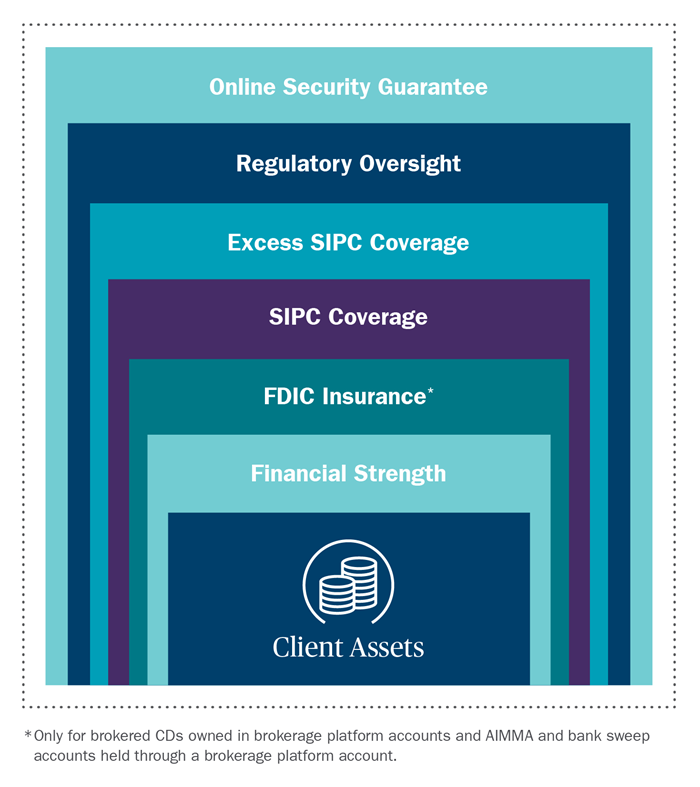

Understanding Sipc And Fdic Coverage Ameriprise Financial

The Menace Of Mis Selling In Insurance And How To Curb It Mint

How Does Life Insurance Work Forbes Advisor

Can Life Insurance Affect Your Medicaid Eligibility

Bank On Yourself Infinite Banking Whole Life Insurance Concept

Bank Owned Life Insurance Boli

Bank Owned Life Insurance Boli

Indexed Universal Life Insurance 2022 Definitive Guide

Top 10 Pros And Cons Of The Infinite Banking Concept How To Become Your Own Banker In 2022

Indexed Universal Life Insurance 2022 Definitive Guide

What Is A Bank And How Does It Work Forbes Advisor

Understanding Sipc And Fdic Coverage Ameriprise Financial

Understanding Life Insurance Policy Ownership The American College Of Trust And Estate Counsel

5 Tips For Selling Your Life Insurance Bankrate

Common Mistakes In Life Insurance Arrangements

Federal Register Regulatory Capital Rules Risk Based Capital Requirements For Depository Institution Holding Companies Significantly Engaged In Insurance Activities

:max_bytes(150000):strip_icc()/hsbc-branch-in-new-bond-street--london-533780165-ff99ebc393c243cba463ea80559836b0.jpg)

Bank Owned Life Insurance Boli

Federal Register Regulatory Capital Rules Risk Based Capital Requirements For Depository Institution Holding Companies Significantly Engaged In Insurance Activities

Federal Register Regulatory Capital Rules Risk Based Capital Requirements For Depository Institution Holding Companies Significantly Engaged In Insurance Activities